In the past few months, FHA loans have become remarkably more attractive, making them a better deal whether you're financing or refinancing your home.

Started by the government in the 1930s, the FHA insurance plan has now been used to guarantee more than 40 million mortgages. That's a lot of public support and there's a reason for it: FHA loans have liberal qualification standards and require little down.

Now, FHA loans have gotten even better. Here's why.

FHA Mortgage Rates

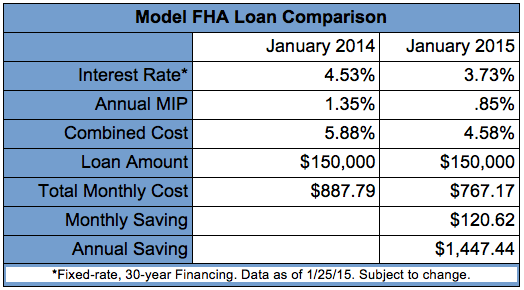

Mortgage rates during the past year have fallen substantially. According to Freddie Mac, at the start of 2014 the typical interest rate for a 30-year fixed-rate mortgage was 4.53 percent, a rate that fell to 3.73 percent in January 2015.

That's a savings of .8 percent. If you borrow $150,000 you will pay $762.70 per month for principal and interest at 4.53 percent, but only $692.97 with the lower rate. With the more recent rate, a borrower in this example will save $69.73 per month or $837 annually.

But wait – as they say on late night television – there's more.

FHA requires its borrowers to take out mortgage insurance. FHA’s mortgage insurance program has two types of fees: An up-front mortgage insurance premium equal to 1.75 percent of the loan amount and an annual mortgage insurance premium equal to 1.35 percent of the outstanding loan balance depending on loan amount, loan term and LTV.

Why get an FHA mortgage? With an FHA-backed loan you can purchase a home with as little as 3.5 percent down, poorer credit and more liberal debt-to-income ratio requirements versus tighter lending requirements that typically come with conventional loans.

Mortgage Insurance Premiums Fall

Beginning Jan. 26, 2015, FHA cut the annual mortgage insurance premium for most new borrowers from 1.35 percent to .85 percent. That's .5 percent less. For a $150,000 loan, it's a savings of about $750 a year.

If you compare FHA loans originated a year ago and those originated today, here's how they stack up for typical borrowers with a $150,000 mortgage.

The FHA Streamline Refinance

But what if you have already financed with an FHA loan? Are the new rates and savings beyond reach?

For many FHA borrowers the answer is no. The FHA Streamline refinance program gives you a financial do-over, which will allow you to get both today's rates and the new and lower annual MIP. To qualify, your current loan must be at least 210 days old and you must have a good payment history. The FHA does not require a credit check or appraisal for the Streamline Refinance program. If your current FHA loan is less than three years old, some of the up-front mortgage insurance premium paid for your existing financing can be applied to your new FHA mortgage.

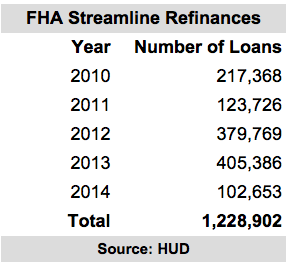

Figures provided to loanDepot by HUD show that 1.2 million borrowers took advantage of the FHA Streamline program during the past five years. This seems like a big number, but that is out of more than 7.7 million current FHA loans.

Millions of FHA borrowers might be able to cut their monthly mortgage costs have yet to take advantage of the Streamline refinancing program. If you have an existing FHA loan, check into the FHA Streamline program. It could be a big money-saver for years to come.

A loanDepot licensed loan officer can help with these and any other lending questions. Call (888) 983-3240 to speak with one today.

Published March 5, 2015

RELATED STORIES

5 ways to benefit from a home refinance

FHA looks to ease rules on lender mistakes

FHA reduces mortgage insurance costs

What NOT to do when refinancing